Major Tax Changes Could Be Coming in 2026: What Small Business Owners Should Know

Key tax provisions for small businesses including the 20% QBI deduction are scheduled to expire after 2025. Learn what North Dakota business owners should watch as 2026 approaches.

Several major tax provisions that have benefited small business owners for the past several years are scheduled to expire after December 31, 2025.

These provisions were originally created under the Tax Cuts and Jobs Act (TCJA) and have played a significant role in reducing taxes for many businesses across the country—including here in North Dakota.

Unless Congress takes action to extend or modify them, 2026 could bring meaningful tax changes for business owners.

The 20% Qualified Business Income Deduction

One of the biggest provisions set to expire is the Qualified Business Income (QBI) deduction, often called the Section 199A deduction.

This deduction allows many owners of pass-through businesses such as:

LLCs

Partnerships

S-Corporations

Sole proprietorships

to deduct up to 20% of their qualified business income.

For many small businesses, this deduction has significantly reduced their overall tax burden.

If the provision expires, business owners could see higher taxable income starting in 2026.

Individual Tax Rates May Increase

The TCJA also temporarily reduced individual tax rates across several brackets.

If these provisions sunset as scheduled, tax rates could revert to pre-2018 levels, which means some business owners may see higher personal tax rates on business income.

Because most small businesses are pass-through entities, these individual rate changes can have a direct impact on business owners.

Estate and Gift Tax Exemption Could Drop

Another major provision scheduled to change is the federal estate tax exemption.

Currently, individuals can pass on over $13 million without triggering federal estate tax. In 2026, that exemption could be reduced roughly in half if the law sunsets.

While this primarily affects larger estates, it could have implications for:

Multi-generational farms

Family-owned businesses

Land transfers

Why Planning Now Matters

Although 2026 may seem far away, tax planning often works best when decisions are made years in advance.

Business owners may want to start thinking about:

Income timing strategies

Equipment purchases and depreciation planning

Business structure reviews

Long-term succession planning

The actual outcome will ultimately depend on what Congress decides, but preparing early can help avoid surprises later.

Staying Ahead of the Changes

Tax laws change regularly, and the next few years could bring significant updates for small business owners.

Keeping an eye on upcoming tax changes and planning ahead can help businesses stay flexible and make informed financial decisions.

For North Dakota business owners, working with an advisor who understands both tax law and local industries can make a big difference when navigating these changes.

Steinke & Company

What Farmers Should Know About 1099 Reporting in 2026

1099 reporting is a common headache for farm operations. Here’s what North Dakota farmers need to know about issuing 1099s to contractors and avoiding IRS penalties.

If you run a farm or ag business, tax paperwork is nothing new. But every year we still see producers run into the same surprise when January rolls around: 1099 reporting requirements.

Whether you hire custom operators, truckers, agronomists, or independent contractors, there’s a good chance some of those payments require a Form 1099-NEC.

And if those forms aren’t issued correctly, the IRS can apply penalties that add up quickly.

When Farmers Must Issue a 1099

Most farm operations must issue a 1099-NEC when they pay $600 or more to a non-employee for services during the year.

Common examples in agriculture include:

Custom combining or spraying

Independent truck drivers hauling grain or livestock

Agronomy or consulting services

Equipment repair by independent contractors

These payments must be reported if the provider is operating as an individual, partnership, or LLC taxed as a partnership.

When You Typically Don’t Need One

There are a few situations where a 1099 usually isn’t required.

You generally do not issue a 1099 if:

The vendor is taxed as an S-Corporation or C-Corporation

The payment was made by credit card or payment processor

The expense was for products rather than services

However, the safest approach is to collect a Form W-9 before paying any new vendor so you know their tax classification.

Why the W-9 Matters

The W-9 tells you:

The vendor’s legal name

Their business entity type

Their taxpayer identification number

Without this information, preparing 1099s in January becomes much harder and sometimes impossible.

Many farmers don’t think about this until the end of the year, when trying to track down contractors who finished work months earlier.

Penalties Are Increasing

The IRS continues to increase penalties for missing or incorrect 1099 forms.

Penalties can range from $60 to $310 per form, depending on how late the correction is made. For farms working with multiple custom operators or service providers, that can add up quickly.

A Simple Habit That Saves Time

The easiest way to avoid 1099 headaches is simple:

Request a W-9 before the first payment is made.

Keeping those forms on file throughout the year makes January reporting much easier and prevents last-minute scrambling.

Planning Ahead

Agriculture businesses often work with a wide range of contractors throughout the season. Taking a few minutes to organize vendor information now can save significant time and stress at tax time.

If you have questions about 1099 requirements, farm tax planning, or ag business structures, working with an accountant who understands agriculture can make a big difference.

Steinke & Company

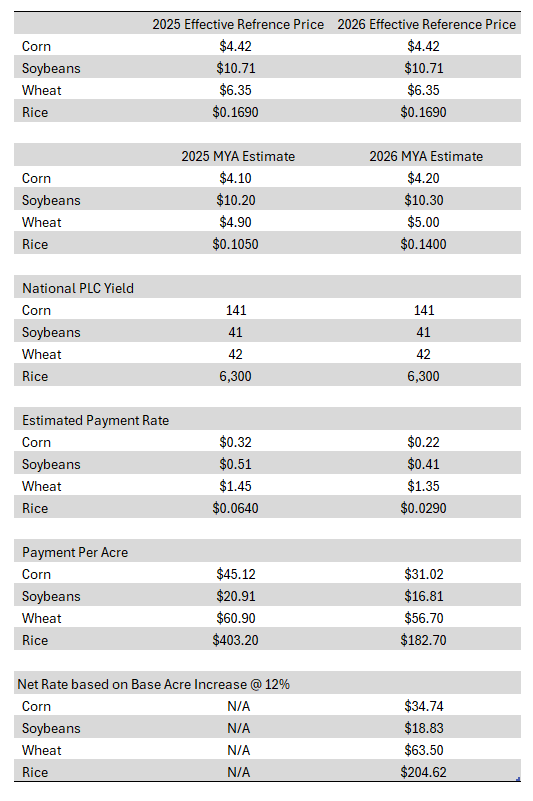

What Might 2026 PLC Payments Look Like?

What could 2026 PLC payments look like? Using USDA Ag Outlook Forum projections, we estimated potential national PLC payment rates for corn, soybeans, wheat, and rice — and early numbers suggest lower rates compared to 2025, with base acre increases partially offsetting the decline. Here’s what that could mean for producers.

Let’s talk farm policy.

We know. Not exactly edge of your seat material. But when it impacts your operation’s cash flow, it gets a lot more interesting.

Last week, USDA released updated projections at the Ag Outlook Forum, including estimated 2026 national MYA (Marketing Year Average) prices for corn, soybeans, and wheat. Those projected MYA prices are what drive potential PLC (Price Loss Coverage) payments.

So we ran some early numbers.

How We Built the Estimate

Using USDA’s projected MYA prices, we calculated preliminary 2026 national PLC payment rates for:

Corn

Soybeans

Wheat

Rice

For rice, we used a 14-cent per hundredweight MYA estimate. As additional MYA projections are released, we’ll continue refining these estimates.

Keep in mind — this is early. These are projections built on price outlooks before most 2026 crops are even in the ground.

What the Numbers Suggest

Based on current USDA projections:

All major crops show a decrease in PLC payment rates compared to 2025.

However, base acres nationally are expected to increase by roughly 12%.

After accounting for that increase in base acres, wheat shows a slight overall increase in total payments compared to 2025.

In other words: payment rates may be lower, but expanded base acres could partially offset the decline.

Important Notes

A few things these numbers do not reflect:

Payments are only made on 85% of base acres (the standard PLC reduction).

Payment limitations are not factored into these estimates.

Actual 2026 MYA prices could change significantly.

And perhaps most importantly — we are very early in the cycle. Final projections will shift as planting decisions, weather, global production, and markets evolve.

What This Means for Producers

Right now, this isn’t about making final decisions. It’s about staying aware.

Lower projected PLC rates may mean:

Tighter safety net support in certain crops

Greater sensitivity to market price swings

More importance placed on crop insurance and marketing strategy

The 12% base acre increase helps, but it may not fully offset declining payment rates depending on how prices develop.

We’ll continue monitoring updates and adjusting projections as new data becomes available.

Because farm policy may be dry — but its impact on your operation isn’t.

If you have questions about how PLC projections affect your farm’s cash flow planning, reach out. We’re watching it closely.

Steinke & Company

Front Office Receptionist (In-Person)

Steinke & Company is seeking a highly organized, tech-savvy Front Office Receptionist & Operations Associate to serve as the face and operational backbone of our Rugby, ND tax and accounting office. This is a fast-paced, client-focused role ideal for someone who thrives on multitasking, follows through without supervision, and takes pride in keeping systems, schedules, and client communication running smoothly.

About the Role:

Steinke & Company is a tax and accounting firm serving agricultural producers and rural small business owners. We are looking for a highly capable Front Office Receptionist & Operations Associate to serve as the face and backbone of our office.

This is not a passive front desk role. This position requires strong customer service skills, solid technology fluency, exceptional memory, and self-directed follow-through. You must be comfortable multitasking in a fast-paced office, managing multiple systems at once, and keeping things moving without constant supervision.

If you thrive in organized chaos, enjoy helping people, and naturally take ownership of tasks until they are complete, this role may be a strong fit.

Schedule Requirements:

May – November: (Off Season)

Monday – Thursday, 9:00am–3:00pm (Central)

December – April (Tax Season): Monday – Friday, 9:00 am–4:00 pm (Central)

Additional hours may be required during peak tax season.

Key Responsibilities:

Front Office & Client Service

Greet clients professionally and warmly in person and by phone

Answer and manage a multi-line phone system

Transfer calls appropriately, take detailed messages, and ensure follow-through

Schedule appointments and manage calendars

Be the first point of contact during tax season

Help clients log into and navigate our secure client portal

Send and track client organizers and tax return deliveries

Maintain professionalism during high-stress client interactions

You must have excellent memory and follow-up habits. If someone calls, emails, or drops something off, it must be handled or tracked until resolved.

Administrative & Office Support:

File management and document organization (Google Drive & internal systems)

Maintain client records accurately

Manage calendars (Acuity & Google Calendar)

Provide general administrative support to the CEO and remote team

Assist with 1099 entry and other seasonal data entry

Support monthly bookkeeping clients (QuickBooks Online)

You must be able to juggle multiple active tasks without dropping details.

Operations & Systems Support:

Use and help maintain our CRM and workflow systems (Canopy)

Help design and implement simple automations

Keep internal processes organized and updated

Assist with onboarding and offboarding clients

Maintain standard operating procedures and templates

You should be comfortable learning new software and troubleshooting basic issues independently before asking for help.

Required Skills & Qualities:

Strong customer service and interpersonal skills

Confident, clear communicator (phone and in person)

Comfortable with technology and cloud-based systems

Excellent attention to detail

Strong memory and task follow-through

Self-directed and able to work independently

Comfortable working in a busy office with multiple interruptions

Able to prioritize and shift quickly between tasks

Professional, calm, and reliable under pressure

Ability to keep privacy and confidentiality for our clients

Preferred (Not Required):

Experience in a tax, accounting, legal, or medical office

Familiarity with QuickBooks Online

Familiarity with client portals or CRM systems

Experience during tax season or other seasonal business cycles

This Role Is NOT For You If…

You need constant instruction or supervision

You avoid phone communication

You struggle with technology

You dislike multitasking

You have difficulty following through on details

You prefer slow, repetitive admin work

You hate people

Why Join Us?

We serve hardworking rural business owners and agricultural producers. Our team values professionalism, initiative, and continuous improvement. We are building systems that support both our staff and our clients.

If you enjoy being the organized center of a fast-moving office and take pride in keeping things running smoothly, we’d love to hear from you.

How to Apply

Send a short introduction explaining:

Your previous administrative or office experience

What software tools you’ve used

How you stay organized when things get busy

An example of a time you had to manage multiple tasks at once

Bonus: Include a short Loom video explaining how you manage tasks or handle difficult client situations.

Job Types: Part-time, Full-time

Benefits:

401(k)

401(k) matching

Dental insurance

Employee discount

Health insurance

Paid time off

Professional development assistance

Retirement plan

Vision insurance

Schedule:

Day shift

Monday to Friday

No nights

No weekends

Supplemental Pay:

Bonus pay

Experience:

Customer service: 4 years (Required)

Ability to Commute:

Rugby, ND 58368 (Required)

Work Location: In person

The Form W-9 Is Not a Personal Attack

A Form W-9 is not a red flag or a trigger for the IRS—it’s a routine business document. This guide explains what a W-9 actually does, how it relates to 1099 reporting, and why refusing to provide one can create unnecessary risk for your business relationships.

Every year, the same thing happens.

A business requests a Form W-9 from a vendor… and the reaction ranges from mild annoyance to full-blown panic.

Let’s clear something up immediately:

A W-9 on its own means nothing.

It does not automatically mean you’re getting a 1099.

It does not “trigger” the IRS.

It is not a conspiracy.

I can’t believe I even have to write this. But inceraisngly, each year, I have to explain that a W9 is not your customer or vendor or the IRS “coming” for you or trying to “track” you.

It is simply a basic information form. It’s existed for years. About 1984 to be exact.

What a W-9 Actually Does

A Form W-9 tells the requesting business:

Who you are

What type of entity you are

And thus how you’re taxed

Where tax forms should be sent if required

That’s it.

Many corporate offices require a W-9 from every vendor as standard procedure. Others use it simply to maintain accurate contact and tax records. It’s routine compliance — not an accusation or a tracking system.

If You’re a Business Owner, You Should Be Collecting Them Too

Here’s the part many people miss:

If you operate a business, you should be collecting W-9s — not just complaining about receiving them.

You need W-9s to properly issue 1099s when required.

And if you ever need to chase payment, enforce a contract, or place a lien, you’ll be glad you already have the correct legal and tax information on file.

This is basic risk management.

“I’m an LLC. I Don’t Need to Fill One Out.”

Yes. You do.

“LLC” is not a tax classification. It’s a state-level legal structure.

For federal tax purposes, an LLC is taxed as one of the following:

Sole proprietor

Partnership

S-corporation

C-corporation

That tax classification — not the letters “LLC” — determines how 1099 rules apply.

The W-9 simply clarifies how you are taxed so the payer knows whether a 1099 is required.

In fact, everyone needs to and should fill out the W9 if it’s requested. Even corporations. Because the person sending it doesn’t know you’re incorporated! Once you send them the form, they’ll know and actually take you OFF their list.

What If You Do Receive a 1099?

A 1099 is not “extra tax.” It is reporting.

The income shown on a 1099 should already be included in your books. On your tax return, that income is offset by legitimate business expenses such as:

Wages paid

Cost of goods sold

Contractor expenses

Operating costs

Many incorporated businesses receive 1099s even when they are technically exempt. It does not change the accounting. It does not automatically increase tax liability. It simply documents income that should already be recorded.

Why This Actually Matters

The IRS does not view W-9s and 1099s as optional paperwork.

There are real penalties for failing to issue required 1099s — and those penalties fall on the business that failed to collect the W-9. You’re not exempt if the person doesn’t respond.

If you refuse to provide one, you are asking your customer to take on unnecessary compliance risk with real monetary penalties.

Most established businesses will not do that.

They will not argue.

They will not chase you.

They will quietly hire another vendor who understands standard business procedures.

We’ve done this. We advise our clients to do this. And we’ve seen clients do this.

Compliance is table stakes for these big companies. If you want corporate contracts or to scale, you need to get over the W9.

Refusing to participate in basic documentation doesn’t make a business look principled. It makes it look risky and immature.

There’s Also a Relationship Cost

Well-run businesses choose vendors who:

Understand basic compliance

Don’t create avoidable risk

Don’t turn routine administration into conflict

Being hostile about standard paperwork is a fast way to lose good clients, not because they’re petty, but because they’re protecting themselves from IRS notices, penalties, and cleanup work they don’t want.

Final Takeaway

If a W-9 feels threatening, that’s usually not a paperwork problem; it’s most likely a systems problem.

Review:

How you’re classified for tax purposes

How your income is being reported

Whether your bookkeeping supports your filings

Compliance work at this stage of business should feel routine and uneventful. If it feels stressful, something deeper likely needs attention.

Clean it up now, before the IRS or your customers force the issue.

At higher levels of business, this isn’t controversial. It’s just how things are done.

And we’re pretty sick of answering these questions and explaining it each year!

— Steinke & Company

2025 Tax Law Changes: What You Need to Know

Big tax changes are here — and this time, they actually matter. The new O.B.B.B. introduces new deductions for tips, overtime, and car loan interest, increases standard deductions and tax credits, and brings major wins for business owners. Here’s what changed and how it could impact your 2025 taxes.

Tax season looks very different this year. Recent legislation introduced sweeping changes that affect workers, families, retirees, and business owners alike. To help cut through the noise, we’ve pulled together the most important updates in one place: what’s new, what’s changed, and what actions you may want to consider.

Our goal is simple: fewer surprises, less stress, and better tax outcomes.

New Worker Deductions You Can Take Without Itemizing

One of the most talked about changes comes from the O.B.B.B., which introduced three brand new deductions available even if you take the standard deduction.

No Tax on Tips

Qualified workers may deduct up to $25,000 in tip income ($12,500 for single filers).

This applies to:

W-2 employees

1099 contractors

Qualified professions

These deductions phase out for higher earners, generally beginning at $300,000 MAGI for married couples and $150,000 for others. There are also rules and restrictions on which type of tips count. Talk to your tax preparer to fully understand the ins and outs of this new rule.

No Tax on Overtime

Employees can now deduct the overtime premium—the amount earned above their regular hourly rate—up to $25,000 ($12,500 for single filers).

Car Loan Interest Deduction

Taxpayers may deduct up to $10,000 in interest paid on loans for new personal vehicles, provided the vehicle’s final assembly occurred in the U.S.

Bigger Deductions for Most Taxpayers

Thanks to expanded deductions, fewer people will need to itemize this year.

Increased Standard Deduction (Now Permanent)

Married Filing Jointly: $31,500

Head of Household: $23,625

Single Filers: $15,750

SALT Cap Relief

The deduction for State and Local Taxes (SALT) has increased from $10,000 to $40,000 for 2025—welcome news for homeowners and taxpayers in higher-tax states.

New Senior Deduction

Individuals age 65 or older receive an additional $6,000 deduction per person. Combined with other increases, this change effectively eliminates federal income tax on Social Security benefits for nearly 90% of recipients.

Expanded Tax Credits for Families

Several credits aimed at families and caregivers were expanded this year.

Child Tax Credit

Increased to $2,200 per child

At least one parent must have a Social Security Number

ITIN-only households no longer qualify

Child and Dependent Care Credit

Credit rate increased from 35% to 50%

Maximum credit:

$1,500 for one child

$3,000 for two or more

Adoption Credit

Up to $17,280 total

Now partially refundable, up to $5,000

Major Changes for Business Owners and the Self-Employed

Business owners will see some of the most impactful updates this year.

100% Bonus Depreciation Made Permanent

Businesses can continue deducting the full cost of qualifying equipment and assets in the year they are placed in service.

Qualified Business Income (QBI) Deduction

The 20% QBI deduction is now permanent, with more favorable phase-out rules for certain service-based businesses.

1099-K Reporting Threshold Reversal

For 2025, 1099-K forms are issued only if both thresholds are met:

More than $20,000 in gross sales

More than 200 transactions

Immediate R&D Write-Offs

Research and Development expenses may once again be fully deducted in the year incurred. This change is retroactive to 2022.

Expiring Tax Credits: Timing Matters

Some popular energy-related incentives are ending earlier than expected.

Electric Vehicle Credits

Credits for new and used EVs expire after September 30, 2025.

Residential Energy Credits

Credits for solar panels, heat pumps, and energy-efficient windows and doors expire after December 31, 2025.

If you’re considering any of these improvements, planning ahead is critical.

Important IRS Administrative Changes

End of Paper Checks

Starting September 30, 2025, the IRS will no longer:

Issue paper refund checks

Accept paper payments

All refunds and payments must be handled electronically. The best thing to do is make your IRS.gov account and log in! You can also use EFTPS and directpay.gov for payments.

Simplified IRS Payment Plans

Taxpayers who owe up to $50,000 can now set up a payment plan of up to 10 years online, without submitting detailed financial statements.

How to Prepare for a Smooth Tax Season

To help avoid delays and unnecessary stress:

Submit documents as soon as they’re available

Inform us of life changes such as job changes, new businesses, home purchases, vehicle purchases, or family changes

Don’t panic over headlines—we’ll apply what matters to your specific situation

Ask questions early rather than late

Have your banking info ready for electronic payments

Log in and take control of your IRS.gov account ahead of time

Tax law may be complex, but navigating it doesn’t have to be. We’re here to handle the details and help you make the most of the opportunities available this year.

If you have questions about how these changes affect you, reach out anytime—we’re happy to help.

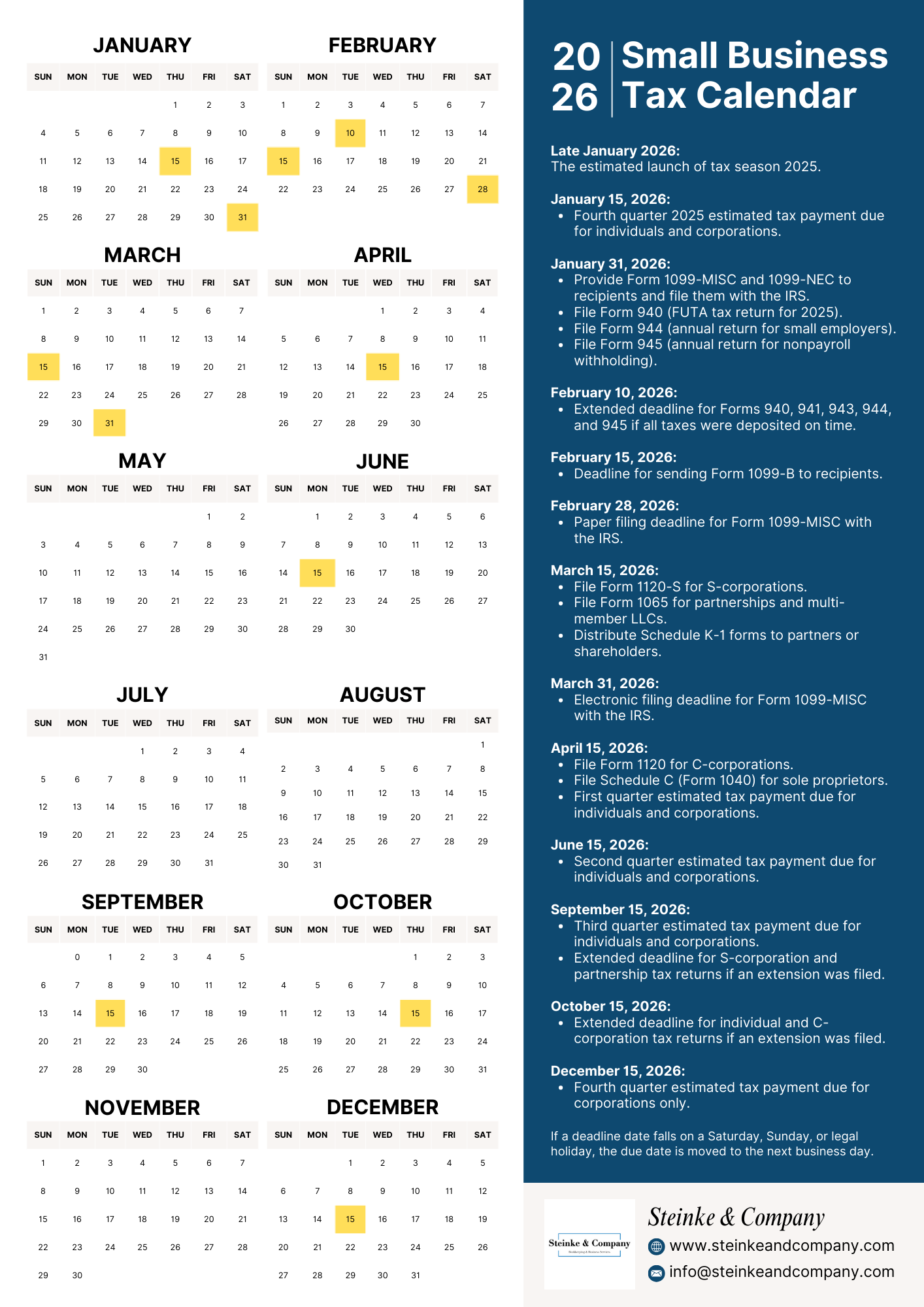

2026 Small Business Tax Calendar: What to Know and How to Stay Ahead

Tax deadlines don’t have to be stressful. This 2026 small business tax calendar breaks down key filing dates, estimated tax payments, and compliance deadlines so you can plan ahead and avoid surprises.

Tax deadlines aren’t just dates on a calendar—they’re decision points that affect cash flow, compliance, and stress levels throughout the year. Whether you’re a sole proprietor, partnership, or corporation, knowing what’s coming allows you to plan instead of react.

Below is a breakdown of the key 2026 small business tax deadlines, along with context on why they matter and who they apply to.

January: Tax Season Begins

Tax season for 2025 returns is expected to open in late January 2026. This is when the IRS begins accepting returns and when missing documents or unresolved issues from the prior year tend to surface.

January 15, 2026

Fourth-quarter estimated tax payments are due for individuals and corporations. This is the final estimate for the 2025 tax year and often catches people off guard after the holidays.

January 31, 2026

This is one of the busiest compliance dates of the year:

Forms 1099-NEC and 1099-MISC must be provided to recipients and filed with the IRS

Forms 940, 944, and 945 are due for applicable employers

Missing this deadline can result in penalties, even if no tax is owed.

February: Payroll & Information Return Follow-Ups

February 10, 2026

An extended deadline applies for certain payroll forms (940, 941, 943, 944, and 945) only if all taxes were deposited on time.

February 15, 2026

Form 1099-B must be sent to recipients.

February 28, 2026

Paper filing deadline for Form 1099-MISC with the IRS.

March: S-Corps and Partnerships

March 15, 2026

This is a critical date for:

S-corporations (Form 1120-S)

Partnerships and multi-member LLCs (Form 1065)

Schedule K-1s must also be issued to shareholders and partners so they can file their personal returns. Delays here often create a domino effect for individual filings.

March 31, 2026

Electronic filing deadline for Form 1099-MISC.

April: A Big One for Many Businesses

April 15, 2026

This date applies to:

C-corporations (Form 1120)

Sole proprietors (Schedule C with Form 1040)

First-quarter estimated tax payments for individuals and corporations

Even if you plan to extend, payment is still due by this date.

Mid-Year Estimated Payments

June 15, 2026

Second-quarter estimated tax payments are due.

September 15, 2026

Third-quarter estimated payments are due, and this is also the extended filing deadline for S-corporation and partnership returns if an extension was filed.

Fall Extensions

October 15, 2026

Extended deadline for individual and C-corporation returns.

Year-End Planning

Year-End Tax Planning

We do these proactive appointments throughout the year, but most people take advantage of them in Q4. Drop off your numbers and we’ll review them and schedule a review call to discuss year-end planning ideas.

December 15, 2026

Fourth-quarter estimated tax payments are due for corporations only. This is often a key point for year-end tax planning and cash flow decisions.

January 15, 2027

Individual estimated payments are due for Q4 of 2026 by January 15. We recommend paying these by Dec 31 now so the IRS doesn’t misclassify the payment to the wrong year. Something they’ve done repeatedly recently.

A Note on Due Dates

If a tax deadline falls on a Saturday, Sunday, or legal holiday, the due date moves to the next business day.

Final Thoughts

Not every deadline applies to every business—but missing the ones that do can be costly. A proactive approach throughout the year makes tax season smoother and allows for better planning, not just compliance.

If you’re unsure which deadlines apply to your business or want help building a system to stay ahead of them, we’re here to help. Contact us below:

— Steinke & Company

Data Security - It's a joke, until it's your info.

Why shouldn’t you send me unsecured documents? I’ll roast you online.

So this morning, a mortgage broker sent me a stranger’s trust document. This afternoon, a real estate title agency asked for my social security number, address, and full name by email. By 2 pm I had lost my cool. These companies are responsible for guarding their client data and doing their jobs without risking your identity with a careless click. My identity isn’t worth it. Unfortunately, Molly didn’t seem bothered that she had sent me the info of a lady in Ohio and that I could see her details, full name, address, and more. Thanks, Molly.

I asked both companies if they had secure portals, and both replied, that they did in fact have these tools. Neither had sent me the link or invite to use them. They just weren’t using them! WTF?

You wouldn’t leave your storefront unlocked overnight, would you? The same care should go into protecting your customers’ sensitive data.

How is a portal different than an email? If Molly had used her portal, she could have deleted or recalled the document and cut off my access. But now that it’s in my email, she can’t get it back. She’s got to rely on me deleting it. I think we all know a creep who wouldn’t delete it. Someone who would be on Facebook looking you up in a second.

That’s where the Gramm-Leach-Bliley Act (GLBA) Safeguards Rule comes in. It’s not just for banks or big corporations—it applies to a wide range of entities, including some you wouldn’t expect. And on June 9 of 2024, further rules went into place, clearly neither of these places are following them.

Here’s the good news: compliance isn’t as overwhelming as it sounds. By the end of this post, you’ll know what the Safeguards Rule is, why it matters, and the simple steps to safeguard your business and customers. You’re small business will be in better shape than these 2 so-called professional companies.

What Is the Gramm-Leach-Bliley Act Safeguards Rule?

The GLBA Safeguards Rule is part of a U.S. law designed to ensure businesses handle sensitive customer information responsibly. It applies to a broad array of entities engaged in financial activities, including:

1. Traditional Financial Institutions:

Banks

Credit unions

Insurance companies

Investment advisors

2. Non-Traditional Entities Engaged in Financial Activities:

Mortgage lenders and closing agents

Financial advisors, lawyers, tax pros

ATM operators, payment processors

Debt collectors

Car rental companies

Courier services

Credit reporting companies

3. Educational Institutions:

Universities and colleges that handle financial activities such as student loans.

4. Other Businesses:

Companies that receive personal information from financial institutions.

Organizations outside the U.S. offering financial services to individuals within the country.

In short, the GLBA applies to any institution "significantly engaged" in providing financial products or services, such as lending, brokering, financial advising, or insurance.

💡 Pro Tip: If your business collects or processes customer financial data in any way, it’s worth double-checking whether the GLBA applies to you. Even if you are just a small business but you have a big client list, or you keep client payment methods on file, you need to check yourself.

Why the GLBA Safeguards Rule Matters for Small Businesses

Imagine this: A small tax preparer skipped encryption to save costs. A data breach exposed hundreds of customers’ personal details, resulting in lawsuits, lost trust, and financial ruin. Or perhaps a mortgage broker sent a trust document to the wrong person, exposing someone’s details to a stranger. Unfortunately, scenarios like this are more common than you’d think:

60% of small businesses close within six months of a major data breach.

Data breaches cost businesses an average of $4.35 million globally in 2022.

Beyond the risks, protecting customer data builds trust, which can set your business apart. When customers know their information is safe, they’re more likely to stick with you.

What’s New in the Updated Safeguards Rule?

Here’s what changed with the most recent updates to the Safeguards Rule:

Encryption Requirements: Businesses must encrypt all sensitive customer information, both in transit and at rest.

Multi-Factor Authentication (MFA): Passwords alone are no longer enough. MFA adds an extra layer of security.

Breach Notifications: If a data breach affects 500+ customers, you must notify the FTC within 30 days.

💡 Keep in mind: These changes are already enforceable, so don’t wait to act. The penalties are also huge and can be loss of licenses, $100,000 fine, and/or 5 years in jail.

How to Make Compliance Simple and Stress-Free

You don’t need a massive IT budget to comply. Follow these three steps to keep things manageable:

1. Develop a Written Security Plan

Think of this as your business’s playbook for protecting customer data. Here’s how:

Identify what types of data you collect.

Determine how and where you store it.

Create a plan to respond to breaches, including FTC notification requirements.

2. Use Affordable Tools

Compliance tools don’t have to break the bank. Here are some recommendations:

Encryption: Tools like BitLocker (Windows) or FileVault (Mac).

MFA: Duo Security offers user-friendly, low-cost solutions.

The Google Authenticator App is free.Use the Security Settings on your Email. You can encrypt emails on Google and other email services offer custom security settings.

Secure Portals: Smartvault and Encyro are easy ways to offer client file sharing.

💡 Helpful tip: Many cloud services include built-in encryption—check your current software for this feature.

3. Train Your Team & Yourself

Make training engaging. Compare phishing emails to “too-good-to-be-true” spam offers or use role-playing scenarios to teach employees how to spot risks. It’s a bit more complicated than “don’t click any links”, but that’s a good start. Take care to choose software vendors who know what they are doing to host your CRM and payment details. Ask your insurance agent what your responsibilities are.

Actionable Checklist to Stay Compliant

Here’s a quick compliance checklist:

✅ Encrypt all sensitive customer data.

✅ Implement multi-factor authentication for logins.

✅ Draft a written information security plan.

✅ Train your employees and yourself on data security best practices.

✅ Set up a breach notification protocol.

✅ Hire an IT consultant if you need more support.

Conclusion: It’s not that hard to get this right.

Protecting customer data isn’t just about avoiding fines—it’s about building trust that keeps your customers coming back.

Start small. A written plan and a few affordable tools can go a long way. And if you need guidance, we’re here to help you secure your business for the future.

💡 Contact us for a consultation on GLBA compliance and data security solutions.

New Small Business Tax School - New Matchmaking Connection!

Today I’m talking about 2 new big things we’ve created to grow our impact and network. Connection Requests and Small Business Tax School.

With tax season approaching, we’ve been busy planning and working on how to make things better for us inside the office but also for our clients. And we’ve been realizing that we just can’t service everyone who needs a tax preparer. We have to focus.

With that giant realization, we’ve created two new things to help us answer your questions, provide better service, and connect people to legit, trusted pros, even if we can’t serve them ourselves.

Small Business Tax School is our new free community, where we’ll post all of our resources, worksheets, checklists, interviews, expert interviews, and business consulting and coaching. When we answer a question, we’ll share it here so that when one learns, all learn. This will help us serve more people faster by being more available in one specific place. It’s impossible to be in all the places simultaneously, and it’s hard only to help one person per hour when you know more people need you and you have a pile of work to do on the desk behind you…… So hop in and get in on the ground floor. It will grow and expand based on what you community wants, so make sure you get your feedback in there.

Our second creation is an offer to connect you with other tax pros and accounting firms who work like us and believe in the power of collaborative and purposeful work. We know we can’t help everyone and are focused on serving our niche because that’s what we do best. But we know many people want to work with someone like us. So we’ve made a quick little form available right here, and when you fill it out, we’ll do the heavy lifting to search our network and then get you a short list of pros who are interested in serving you and are taking new clients just like you. This works for bookkeepers and tax pros alike. So click on our Connection Request and request a Connection!

We hope that these two things can help us serve our clients and community better.

If you are a tax pro or bookkeeper who wants to be considered part of our Connection Network, let us know!

If you hate our new ideas, let me know, too. I’m curious to hear how people think we should deal with the shortage of tax pros, retiring accountants, and an overall deluge of work and demand, especially if you think we’re doing it wrong. I’d like to hear what you’d do. But be careful; we’re hiring, so you may just get asked to join the team.

Email me at stephanie@steinkeandcompany.com

Avoid the Trap: Smart Strategies to Prevent Costly Penalties from Underpaying Estimated Taxes

Underpayment penalties are a common concern for taxpayers, and many are unaware of how substantial they can be. These penalties are assessed by the Internal Revenue Service (IRS) when taxpayers fail to pay enough of their tax liability through withholding or estimated tax payments throughout the tax year. The interest rate for underpayments has been 8% per year, compounded daily, since October 1, 2023 and at least through June 30, 2024. That is up from 3% just two or three years ago.

Understanding underpayment penalties and the strategies to avoid them can save you from unnecessary financial stress and penalties. This article will delve into the intricacies of underpayment penalties and offer guidance on how to navigate these waters effectively.

Understanding Underpayment Penalties - Underpayment penalties are essentially the IRS's way of ensuring that taxpayers are paying their taxes on a quarterly basis rather than waiting until the tax filing deadline. The IRS requires that you pay at least 90% of your current year's tax liability or 100% of the tax shown on your return for the previous year (110% if you're considered a higher-income taxpayer) throughout the year. If you fail to meet these thresholds, you may be subject to the underpayment penalty. Think of it this way: the IRS is effectively charging you interest on the tax money you kept instead of sending it to the government.

The penalty is calculated on a quarterly basis, meaning that if you underpaid in any given quarter, you might be penalized for that quarter even if you overpaid in another. The rate of the penalty is determined by the IRS and can vary from quarter to quarter. For self-employed individuals or those without sufficient withholding, estimated tax payments are a critical tool in managing tax liability and avoiding underpayment penalties. You would think that a quarter of the year would be 3 months, but for the purpose of this calculation, the “quarters” are uneven and cover January – March (3 months), April and May (2 months), June, July and August (3 months) and finally the last 4 months of the year.

De Minimis Exception - The de minimis exception is one way to avoid underpayment penalties. If your total tax liability minus your withholdings and tax credits is less than $1,000, you won't be subject to underpayment penalties. This rule is particularly beneficial for taxpayers who have a relatively small tax liability.

Safe Harbor Payments - Safe harbor payments are essentially benchmarks set by the IRS that, if met, protect taxpayers from underpayment penalties, regardless of their actual tax liability for the year. These benchmarks are designed to ensure that taxpayers pre-pay a minimum amount of their tax obligation throughout the year, either through withholding or estimated tax payments.

The general rule for safe harbor payments requires taxpayers to prepay the lesser of 90% of the current year's tax or 100% of the previous year's tax. However, for those with an adjusted gross income (AGI) over $150,000 ($75,000 if married filing separately), the rules tighten. These individuals must pay the lesser of 90% of the current year's tax or 110% of the previous year's tax to qualify for this safe harbor. Thus, the safe harbor that works for any eventuality is 110% of the previous year's tax liability. In addition, if you had no tax liability in the prior year, then you are exempt from an underpayment penalty.

Since these pre-payments consist of both withholding and estimated tax payments, the timing of these payments is also critical for payments to qualify for the safe harbor penalty exception. Estimated tax payments are due in four installments: April 15, June 15, September 15, and January 15 of the following year, approximately 2 weeks after the end of the “quarters” noted above. If any of these dates falls on a Saturday, Sunday, or legal holiday, the due date will be the next business day. Caution: Some states have different estimated payments dates and, in some cases, amounts for state estimated payments.

Withholding - Unlike estimated payments, withholding is considered paid evenly throughout the year, regardless of when it occurs. This can be particularly useful for taxpayers who realize they may fall short of their safe harbor requirements as the year progresses and boost their withholding by one means or another depending upon the increase required.

An employee can increase their withholding for the balance of the year by providing their employer with a modified W-4 form that will cause the employer to increase withholding for the balance of the year.

Where the increased withholding need is discovered closer to the end of the year, a cooperative employer might be willing to withhold a lump sum amount.

10% is the default withholding rate for nonperiodic withdrawals from traditional IRA accounts when you fail to provide a Form W-4R to the payer that indicates your desired withholding rate (0% - 100%). Thus by submitting a Form W-4R, or a revised one, to the payer of the IRA, requesting a higher withholding rate, additional withholding can be achieved. Where you are not employed (or even if you are), you can create more tax withholding by taking a distribution and then rolling the distribution amount back into the traditional IRA or a qualified retirement plan within the statutory 60-day time frame. To achieve this strategy you will need to make up for the withholding with other funds when making the rollover and make sure you did not have another rollover in the prior 12 months since taxpayers are only allowed one IRA rollover in a 12-month period.

Form W-4R is also used to advise payers of an eligible rollover distribution from an employer retirement plan of the desired withholding rate if it is other than the default rate of 20%.

Form W-4P should be completed to have payers withhold the correct amount of federal income tax from the taxable portion of a periodic pension, annuity (including commercial annuities), profit-sharing and stock bonus plan, or IRA payments. Periodic payments are made in installments at regular intervals (for example, annually, quarterly, or monthly) over a period of more than 1 year.

Calculating the Penalty – If you file your return, owe more than $1,000 and don’t meet an exception, the IRS will compute the underpayment penalty and bill you for it. However, IRS Form 2210 (2210-F for farmers and fishers) can be used to calculate the required annual payment and determine if you have underpaid in any quarter of the tax year. The form considers the amount of tax owed, estimated tax payments made, and any withholding. It then calculates the penalty based on the underpayment for each quarter until the due date of the tax return or until the underpayment is paid, whichever comes first.

If your income varies significantly throughout the year, the annualized income installment method can help reduce or eliminate underpayment penalties. This method allows you to calculate your tax liability and corresponding estimated payments based on your actual income for each quarter, rather than assuming an even income distribution throughout the year.

Farmers and Fishermen - There are special estimated tax requirements for farmers and fishermen. Farmers and fishermen, with at least two-thirds of their gross income for the prior year or the current year from farming or fishing, have two options:

They may pay all their estimated tax by January 15th (which is the 4th quarter due date for estimated taxes), or

They can file their tax return on or before March 1st and pay the total tax due at that time.

The required estimated tax payment for farmers and fishermen is the lesser of:

66 2/3% of the current year’s tax, or

100% of the prior year’s tax.

These provisions are designed to accommodate the unique income patterns of farmers and fishermen, who may not have steady income throughout the year and often realize the bulk of their income at specific times of the year.

Navigating the complexities of underpayment penalties requires a proactive approach to tax planning and payment. By understanding the rules and utilizing strategies such as adjusting withholdings, making estimated tax payments, and taking advantage of the safe harbor rule and the de minimis exception, taxpayers can avoid the financial sting of underpayment penalties. Remember, the goal is to manage your tax liability throughout the year effectively, so you're not caught off guard come tax season.

If you're unsure about your tax situation, please contact this office for personalized advice and peace of mind.